MCLEAN, Va., Sept. 24, 2018 (GLOBE NEWSWIRE) — Even with slightly improving inventory conditions and relenting home price pressures, home sales this year are now expected come in just below last year’s level, according to Freddie Mac’s (OTCQB: FMCC) September Forecast.

MCLEAN, Va., Sept. 24, 2018 (GLOBE NEWSWIRE) — Even with slightly improving inventory conditions and relenting home price pressures, home sales this year are now expected come in just below last year’s level, according to Freddie Mac’s (OTCQB: FMCC) September Forecast.

Although the U.S. economy and job market are firing on nearly all cylinders, the housing market has essentially stalled. Weaker affordability, homebuilder constraints and ongoing supply and demand imbalances over the summer resulted in fewer home sales and less home construction compared to earlier this year.

Freddie Mac expects many prospective homebuyers to continue to have difficulty reaching the market through the rest of the year. Total home sales (new and existing) are now forecasted to decrease 0.9 percent, and home price growth is expected to moderate to 5.5 percent.

“The spring and summer home buying and selling season ultimately ended up being a letdown, despite a faster growing economy and healthy demand for buying a home,” said Freddie Mac Chief Economist Sam Khater. “Unfortunately, too many would-be buyers continue to be tripped up by not enough affordable supply and the one-two punch of much higher home prices and mortgage rates.”

Added Khater, “Prospective buyers are being squeezed the most where demand is the strongest: the entry-level portion of the market. While price appreciation is welcomingly starting to ease in many markets, weakening affordability continues to hamper overall activity.”

Forecast Highlights

- The U.S. economy during the second quarter grew at its fastest pace (4.2 percent) in nearly four years. Solid consumer spending and business investment should keep the economy on a very strong growth path of 3.0 percent this year.

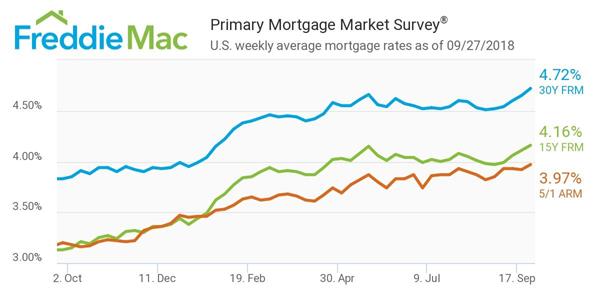

- Mortgage rates inched backward over the summer, but have most recently started to trend higher again. Overall, the 30-year fixed-rate mortgage is expected to average 4.5 percent this year and 5.1 percent in 2019.

- Weakening affordability and not enough moderately-priced homes on the market continue to affect housing activity. Total home sales (new and existing) are now forecasted to decline modestly this year to 6.07 million (6.12 million in 2017), while prices are expected to moderate, but still at a pace above inflation.

- Decreasing refinance activity and home sales from a year ago are expected to cause single-family first-lien mortgage originations to slide around 9 percent this year to $1.65 trillion.

- The share of cash-out refinances last quarter was the highest since the third quarter of 2008 (78 percent). However, the total dollar volume of cash-out refinance activity remains much lower than the peak seen more than a decade ago. An estimated $15.5 billion in net home equity was cashed out last quarter, which is substantially less than the peak cash-out refinance volume of $102.3 billion in the second quarter of 2006.

Freddie Mac makes home possible for millions of families and individuals by providing mortgage capital to lenders. Since our creation by Congress in 1970, we’ve made housing more accessible and affordable for homebuyers and renters in communities nationwide. We are building a better housing finance system for homebuyers, renters, lenders, investors and taxpayers. Learn more at FreddieMac.com, Twitter @FreddieMac and Freddie Mac’s blog FreddieMac.com/blog.

MEDIA CONTACT: Adam DeSanctis

703-903-2786

Adam_DeSanctis@freddiemac.com

A photo accompanying this announcement is available at http://www.globenewswire.com/NewsRoom/AttachmentNg/dd173e75-3bac-4f90-ac02-dbdbab16983f

I just love this image and had to use it. It has been way too long since I used it in an actual post.

I just love this image and had to use it. It has been way too long since I used it in an actual post.

California Gov. Jerry Brown on Sept. 29 signed SB 70, legislation that allows the state’s appraisers to name intended users other than a client in a restricted appraisal report.

California Gov. Jerry Brown on Sept. 29 signed SB 70, legislation that allows the state’s appraisers to name intended users other than a client in a restricted appraisal report.