Have you noticed a significant decline of lender work over the past few months? Do you want to learn how to get more appraisal orders and finally get off the Appraisal Management Company roller coaster ride for good?

Like many appraisers I have seen a very significant decline in AMC orders over the past few months. I have been kicking myself in the butt for not getting started on my marketing to Attorneys, bail bond companies and credit unions prior to the interest rates going up.

Luckily I have a steady stream of attorney work that keeps me busy due to having a good contact management system in place and a steady client base of bail bond companies that refer their customers to me.

In this book I have detailed the steps that I take to create an inexpensive mailer to get more work from credit unions, attorneys and bail bond companies as well as the systems I use to continually get more referral work from all my past clients.

This is an incredible resource to those appraisers that are really looking to learn how do market your appraisal company and build up your client base so you don’t have to deal with seasonal and economic slow downs. This kind of work never goes away!

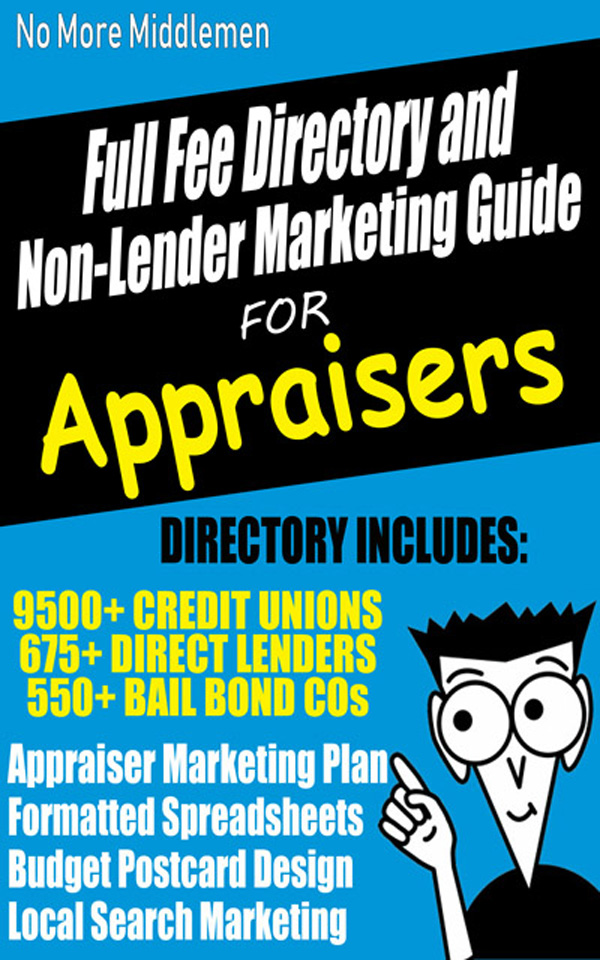

Possibly one of the most valuable aspects of this book is the spreadsheets that include:

9500+ Credit Unions

650+ Bail Bond Companies

350+ Direct Lenders

Click Here To Order

Chapters Include:

- Appraiser Marketing Plan

- 2019 Industry Outlook

- How To Use the Spreadsheets Included With This Book

- Will Rising Interest Rates Affect Your Appraisal Business?

- Getting Off The Appraisal Management Company Roller Coaster Ride for Good

- How to Market to Attorneys, Bail Bond Companies, Direct Lenders and Credit Unions

- Step-by-Step Instructions to Make a Postcard Mailer From Card Design to Mailing

- How To Get Low Cost Mailing Lists Made Targeting Local Divorce and Bankruptcy Attorneys

- Tested Methods on How To Get More Referral Work From Past and Existing Clients

- How to get a FREE Local Listing in Google and Optimize it for Best Results

You are going to especially love the Bail Bond marketing information. These orders are amazing and I have been focusing a lot of my efforts to getting more of their referrals. Why?

When I am referred a customer, I quote 3 fees. I base my first fee off of complexity of the appraisal. Lets say it is a standard tract home in San Diego. I quote them $400 and will inspect within 2 working days and have the appraisal report back to them within 2 days. The second fee is to inspect within 24 hours and have back within 24 hours for $800, and finally a same day inspection and deliver of the appraisal is $1200.

Which one do you think the client wants when they are trying to get a loved one out of jail? 75% of the time it is the $1200 fee for a simple tract home appraisal.

But you do have to follow up to keep these clients, and I have listed all the techniques I use to stay in contact with these clients so the work doesn’t go away.

This resource is jammed packed with information and the spreadsheets are 100% sortable by state to make it easy to create your postcard and do your mailing as noted in Chapter 5: Step-by-Step Instructions to Make a Postcard Mailer From Card Design to Mailing

The next chapter lays out the steps I use to get a massive list of Attorneys in my market area by an inexpensive virtual assistant.

Take the time today to order my New Book & Directory – No More Middlemen – Full Fee & Appraisal Managment Free : 2019 Appraiser Marketing Guide and List of 11000+ Direct Lenders, Credit Unions and Bail Bond Companies and finally get off the crappy appraisal management company roller coaster ride for good!

Click Here To Order

Bryan Knowlton

Appraiser Income

http://www.appraiserincome.com